Formalising Insurance for Rain-Fed Agriculture

Agriculture in Ghana is predominantly rain-fed and dominated by smallholder production systems, with 90–95% of farmers cultivating 2 hectares or less. Farmers operate under significant climatic uncertainty, where a single drought, flood, or pest outbreak can eliminate seasonal income. Rural households rely heavily on what they produce on their farms for both food and income. This means that when farming activities are affected by adverse conditions, their livelihoods are immediately threatened, increasing their chances of falling deep into poverty.

In most farming communities in Northern Ghana, such as Tamale, Savelugu, Bolgatanga, Wa, and Bawku, where crops such as maize, millet, sorghum, groundnuts, rice, and soybeans are widely cultivated, farmers are currently facing escalating setbacks due to increasingly unpredictable weather patterns. Many smallholder farmers are struggling to adapt to these harsh conditions, raising concerns about livelihoods and economic stability in the country’s agricultural sector.

According to Abdulai, a maize farmer in Ejura, when the rains arrived late last season, many farmers waited, replanted, and waited again, and some fields never recovered. For farming households, the losses were not only agricultural but also financial and nutritional. The season exposed how vulnerable smallholder production is to weather variability. “The crops came up well, then the rain stopped for weeks,” he said. By the time rainfall returned, much of his field had dried out. He estimated he lost more than half his harvest and said replanting was not realistic for many farmers because of the cost of seed and fertilizer.

In the Savannah Region, particularly in Central Gonja and Sawla Tuna Kalba districts, many farmers planted after the first rains in May, expecting the usual steady pattern to follow. Instead, long dry spells set-in mid-season. Fields that had germinated well began to wither. Local agriculture officers reported significant maize and millet losses across several communities.

While farmers adapt in the ways available to them, such as adjusting planting dates, many say these efforts alone are not enough to shield them from increasingly frequent climate shocks. A single failed season can wipe out months of investment in seed, fertilizer, and labour, leaving households indebted and vulnerable. In districts where rain-fed agriculture remains the backbone of the local economy, the absence of a reliable safety net means farmers bear the full weight of weather-related losses.

With rainfall becoming more unreliable each season, pressure is mounting for practical and affordable agricultural insurance schemes that truly meet the needs of smallholder farmers. Advocates argue that such coverage would not only compensate farmers after climate-related crop failures but also stabilise incomes and give them the confidence to invest in better inputs, such as high-yielding seed varieties.

Ghana formalised this effort through the establishment of the Ghana Agricultural Insurance Pool, a multi-insurer arrangement designed to provide weather index insurance for smallholders and multi-peril insurance for commercial farms.

Weather Index Insurance: How It Works for Crop Producers

Weather index insurance (also known as parametric insurance) is designed to protect farmers against losses caused by extreme weather conditions. Unlike traditional crop insurance, which requires field inspections to assess actual damage, weather index insurance relies on measured weather data, such as rainfall or temperature, collected from meteorological stations or satellite systems. When conditions exceed predetermined thresholds, payouts are automatically triggered.

For smallholder farmers, this system offers a simpler and faster alternative to conventional insurance. For example, if rainfall during a critical planting period drops below an agreed level, the policy automatically compensates insured farmers, even without visiting individual farms. This reduces delays, administrative costs, and disputes over damage assessments. In areas where farming depends heavily on rainfall, this type of insurance can provide financial relief in a timeframe that facilitates rapid replanting or recovery.

In an interview with our team this year, Sarah Yanume Beinpuo, Manager of Agricultural Insurance at Quality Insurance Company (QIC), explained that the company entered Ghana’s agricultural insurance market in 2018 with a drought index product, which was later expanded in 2020 into a weather index insurance scheme covering both drought and excess rainfall risks. The revision aimed to better reflect evolving climate realities, where farmers increasingly face alternating dry spells and heavy rainfall events.

She noted that QIC prioritizes direct engagement with farmers, particularly through associations and aggregators, using group meetings and targeted outreach to build understanding and trust around insurance products. According to her, the parametric nature of the product has strengthened farmer confidence, as payouts are triggered automatically based on weather data rather than field inspections. In several cases, insured farmers received compensation within ten days of a trigger event, reinforcing positive perceptions of agricultural insurance as a timely risk-management tool.

Image of satellite-linked rain gauge and weather station by Robert_Ford from Getty Images

A Safety Net Only Few Farmers Know About

Despite the growing availability of agricultural insurance products in Ghana, awareness among smallholder farmers remains limited. In many rural communities, particularly across the northern regions, conversations about climate adaptation often center on changing planting dates, switching crop varieties, or relying on informal support networks. Insurance, though increasingly promoted as a financial buffer against weather shocks, is still unfamiliar territory for many farmers.

Our interactions with farmers reveal that while some have heard of agricultural insurance, few fully understand how it works. Many associate insurance with motor vehicles or urban businesses, not crop production. Others express uncertainty about how payouts are triggered, how premiums are calculated, or whether compensation will actually be delivered when losses occur.

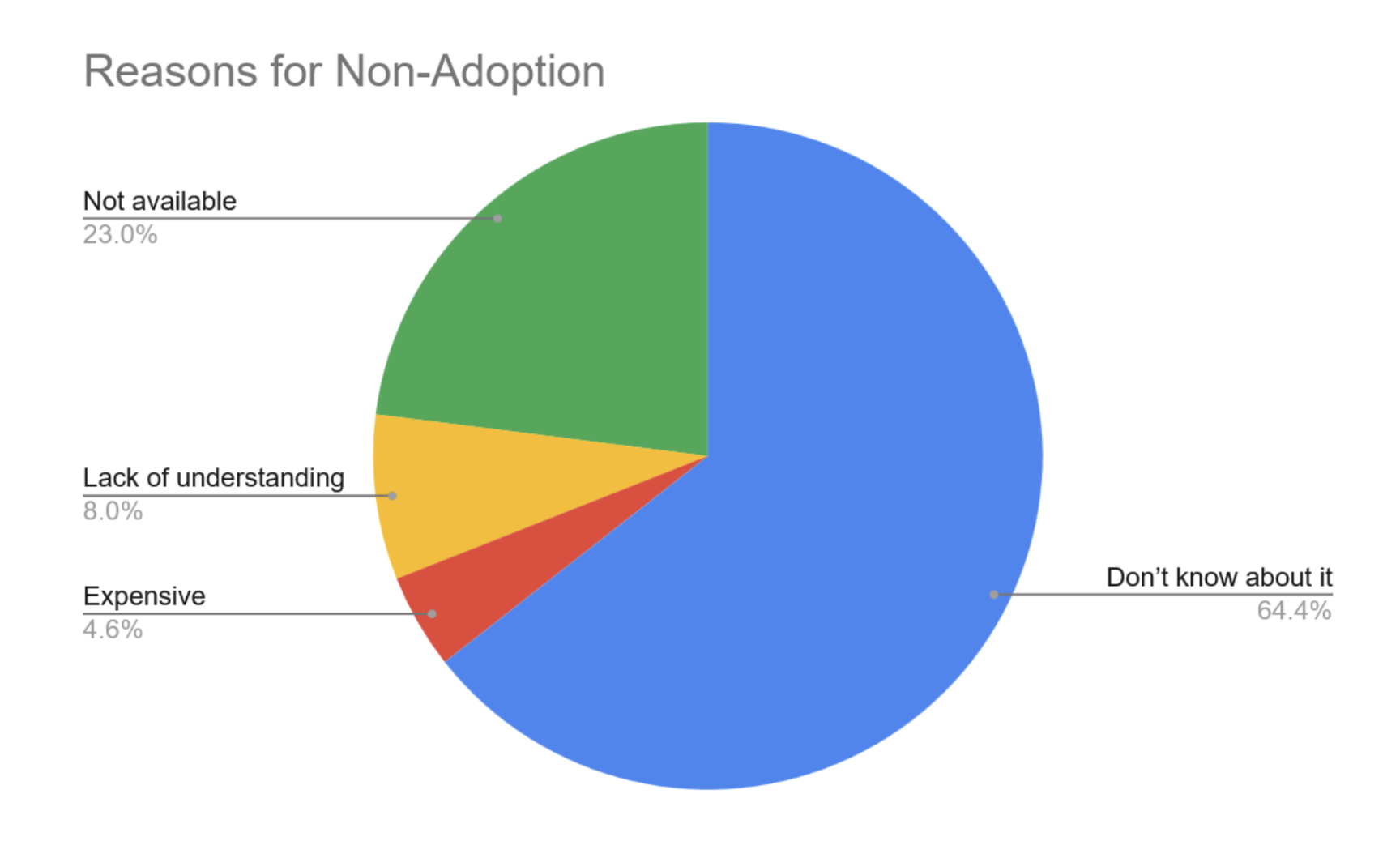

A study covering 200 smallholder farmers across the Northern, Volta, and Western Regions of Ghana found that only 14% of farmers had access to or had adopted agricultural insurance products. Additionally, 64% of respondents identified inadequate knowledge of agricultural insurance products as the main reason for not subscribing, indicating that limited awareness and understanding are major barriers to uptake.

A further 23% of respondents reported that agricultural insurance products were not available to them even when they needed them, suggesting structural and distribution challenges within the insurance market. A smaller proportion of farmers cited financial constraints as a barrier, with 4.6% stating that insurance premiums were too expensive. Furthermore, 8% of respondents mentioned other related factors such as lack of funds and limited understanding of how insurance policies work.

Insurance providers often rely on farmer associations, aggregators, or financial institutions to distribute products. Farmers who are not part of organised groups may never encounter these offerings. In more remote communities, limited engagement between insurers and farmers further deepens the awareness gap.

The cost of premiums remains a significant barrier to adoption, as many smallholder farmers perceive agricultural insurance as an added financial burden on already limited seasonal budgets. One of the farmers we interacted with expressed concern that even when premiums fall within their stated willingness-to-pay range, most farmers prioritise immediate farm inputs such as seeds and fertilizer because the benefits of insurance feel uncertain. As a result, insurance is often treated as a secondary expense rather than an essential part of production.

Farmers’ hesitation to adopt insurance reveals a broader question: who ultimately carries agricultural risk in Ghana’s farming economy? Beyond farmers themselves, financial institutions and risk-sharing organisations play a critical role in shaping how risk is distributed across the sector.

Is Risk Protection the Key to Agricultural Resilience in Ghana?

One of the organisations providing innovative financial solutions to support agri-businesses in Ghana is GIRSAL, which provides agricultural credit risk guarantees to around 40 agricultural lending institutions. These guarantees serve as a form of collateral, encouraging banks to extend credit to farmers. This unlocks capital for crop production, aggregation, and value chain activities.

According to Mr. Tagbotor, Chief Risk Officer at GIRSAL, the most significant and persistent threat facing Ghanaian farmers is the unpredictability of weather. Heavy dependence on rain-fed agriculture makes farmers highly vulnerable to droughts and erratic rainfall.

When discussing agricultural insurance, Mr. Tagbotor emphasized that penetration in Ghana remains very low. Key barriers include high premium costs, limited farmer education and awareness, and concerns about timely payouts when risks materialise. While GIRSAL does not require insurance as a condition for its guarantees, banks may request additional insurance coverage. However, due to cost constraints, GIRSAL does not actively recommend it in most cases.

Mr. Tagbotor noted that for agricultural insurance to become more viable and impactful, premium subsidies or grant-based support may be required. Without financial backing to reduce the burden on farmers, widespread adoption remains unlikely.

From our findings, farmers who have experienced crop failure are more likely to insure because they understand the financial consequences of production risk. This also depends on the size of the farm. When insurance is bundled with agricultural loans, uptake increases because farmers associate insurance with credit eligibility rather than risk management. Farmers often value access to loans more than insurance itself. When insurance is a prerequisite for obtaining credit, they perceive it as part of the loan package rather than as a separate financial product. In bundled models, insurance protects the lender and enables borrowing. In addition, insurance premiums are often deducted directly from the loan amount.

Farmer Experience with Agricultural Insurance: Insights from an OCP Africa Producer

Eric Nesta Quarshie, a farmer participating in an agricultural insurance scheme, provided insights, from a user perspective, into how insurance operates within real farming systems in Ghana and how producers perceive its value amid rising climate uncertainty.

Managing large-scale production activities at OCP Africa that include approximately 50 acres each of rice and soybean, alongside about 500 acres of maize cultivated through a community farming arrangement. OCP Africa partners with farmers and other key stakeholders to build local production capacity in the countries where it operates.

According to Eric, weather variability has significantly disrupted farming operations in recent seasons. Climate-related shocks, particularly drought and flooding, have emerged as the most severe risks affecting productivity. These events interfere with planting schedules, reduce yields, and create uncertainty around investment planning, making agricultural production far less predictable than in previous years.

In his view, agricultural insurance is no longer optional, describing insurance as becoming “mandatory in every agricultural production,” highlighting a growing recognition among farmers that climate change has transformed agriculture into a high-risk enterprise. Insurance is therefore perceived as a core component of modern farm management rather than simply a financial add-on.

Eric considers the insurance premiums affordable within a corporate-supported farming structure, but recognised that affordability remains a significant barrier for smallholder farmers. This contrast illustrates a persistent equity gap: commercial or institutionally backed producers can access risk protection more easily, whereas many smallholders remain excluded due to cost constraints.

Following production losses caused by both drought and flooding, compensation was received within a few months and the claims process was described as relatively straightforward. This experience suggests that procedural barriers, often cited as challenges in agricultural insurance uptake, were minimal in this case. However, despite the smooth claims process, the payout was insufficient to fully offset production losses. As a result, insurance did not substantially reduce overall financial risk exposure, because payouts cover only a limited portion of production costs, farmers must still exercise caution when expanding operations.

Operationally, Eric reported no major difficulties with the insurance program itself. However, he identified two primary constraints limiting wider adoption among farmers: limited understanding of how agricultural insurance functions and the difficulty many producers face in paying premiums. These challenges, he noted, continue to slow uptake despite growing awareness of climate risks.

To improve adoption, Eric recommended reducing premium costs while strengthening farmer education and sensitisation efforts. Improved outreach and clearer communication, would enable farmers to better understand coverage conditions, claims mechanisms, and the long-term value of insurance as a risk management tool. He also pointed to an important limitation in current insurance design; coverage tends to focus mainly on drought and flooding, leaving other production risks insufficiently addressed. Emphasising the need for insurance schemes to broaden their scope.

Conclusion

Climate risk is no longer an abstract concern for Ghanaian farmers; it is already shaping how they make decisions each season. Our discussions with industry actors suggest that agricultural insurance alone cannot resolve these vulnerabilities. Uptake depends on trust, affordability, farmer education, and stronger integration with agricultural finance and extension systems.

Trust and affordability, however, are closely linked to how insurance is delivered. For insurers, it is rarely economical to sell parametric products to individual smallholders; viability depends on reaching thousands of farmers at scale. As a result, successful models often work through aggregators such as farmer associations, cooperatives, and trusted private-sector actors like OCP Africa. These intermediaries reduce transaction costs by working with large groups of farmers and help build trust in the product, making premiums more affordable and increasing farmers’ confidence in the scheme.

Without these supporting conditions, insurance risks remaining a promising solution accessible only to a limited group of farmers, mostly large-scale commercial producers, rather than a widespread tool for strengthening resilience across Ghana’s farming sector. More coordinated interventions are therefore needed to support all-round agricultural resilience.

Paul Temidayo

Independent Researcher for Resilience Constellation